Rate Hike Risk Is Back: What Happens To Your Borrowing Power If The RBA Moves In February

If the RBA lifts rates in February, most people assume it just means higher repayments.

That’s the obvious part.

The bigger issue is borrowing power — because banks don’t assess you at your current rate. They assess you at a stress-tested rate, and that’s the difference between being “pre-approved” and actually being able to buy the next property you want.

Right now, the cash rate is 3.60%, and the next update is due 2:30pm AEDT, 3 February 2026. (Reserve Bank of Australia)

Lenders have already started moving, with fixed rates lifted by major banks ahead of the meeting. (News.com.au)

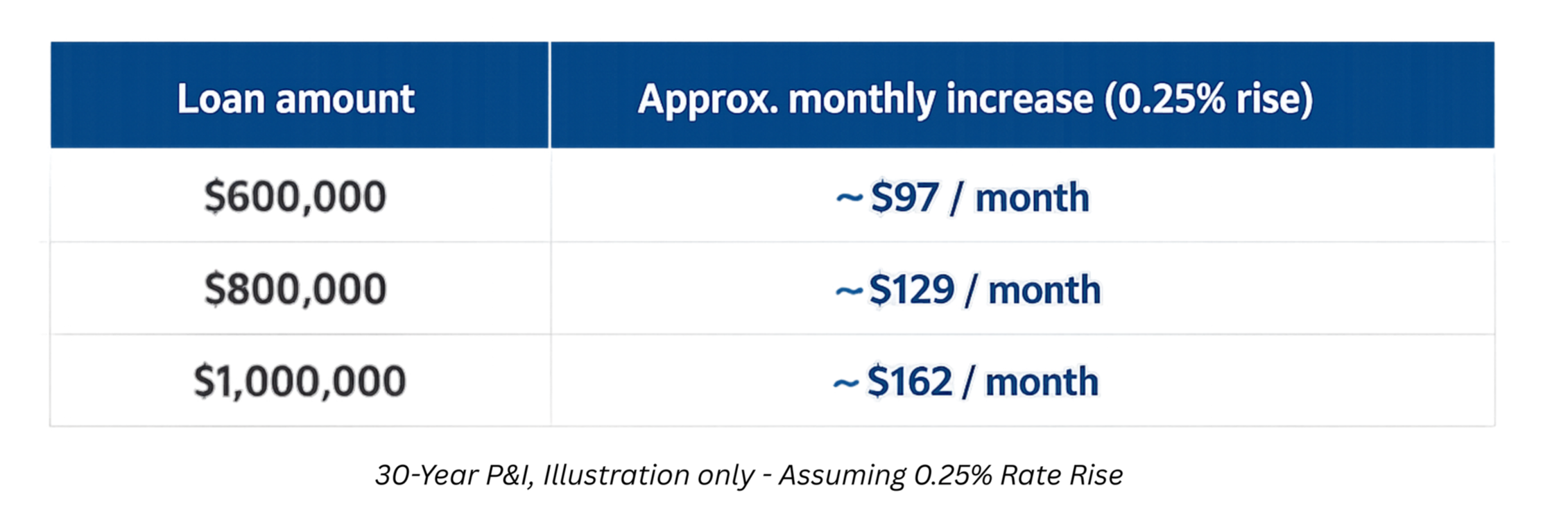

Why a 0.25% hike can change your buying plan

A rate move hits you two ways:

1) Repayments rise

2) Borrowing power drops (this is the real damage)

APRA’s serviceability buffer is +3% and still applies. (apra.gov.au) - So you’re not assessed at your actual rate - you’re assessed higher.

Example: if your actual rate is ~6.25%, a lender may assess you closer to ~9.25% (varies by lender).

When rates rise, that assessment rate rises too - which means:

Serviceability shrinks

Maximum loan size reduces

Your price range can drop overnight

That’s why rate moves don’t just affect repayments - they can change what you’re allowed to buy.

Pre-approval isn’t protection

A pre-approval isn’t a guarantee because:

It can be reassessed

Servicing can be re-run if rates/policy changes

The real test is credit at purchase time

In a tightening market, you don’t want “pre-approved”.

You want “positioned” — with a plan that still works if the goalposts move.

February 2026 is a double squeeze (rates + DTI)

From 1 Feb 2026, APRA’s DTI limits begin: banks can only write up to 20% of new lending at DTI ≥ 6 (separately for investors and owner-occupiers). (apra.gov.au)

Plain English:

High-DTI borrowers become limited capacity

Lenders get pickier and conditions increase

Borderline approvals slow down or fall over

A small rate move can push you into the “harder to place” bucket

What you’ll actually see when hike risk rises

When hikes are in the air, this is what happens:

Banks move early (fixed rates often shift first)

Borrowing calculators tighten quietly

Credit teams dig harder (more docs, more conditions, more time)

Borderline deals stop working — not because the property is bad, but because finance gets harder to land

And buyers who aren’t ready get forced into bad outcomes:

smaller budget → compromised asset

“cheap” stock → higher risk

rushed purchase → overpaying or accepting bad terms

What smart investors do now

Check borrowing power across multiple lenders

Same borrower, different lender = different result. Policy matters.Remove servicing drag

Cut card limits, clean up consumer debt, structure liabilities properly, simplify the file.Avoid thin deals

If it only works if rates fall, it’s not a strategy — it’s a gamble.Hold buffer

Offsets and liquidity protect you when credit tightens.

Want clarity on your borrowing power before the market reprices it?

If you’re planning to buy soon (or build a portfolio), we can run a quick scenario review with our trusted partners and give you a clear buying range that still works if the RBA moves.

Book a chat with the team.